In the first half of 2024, the welded steel pipe industry experienced the most challenging six months in recent years. The international situation remained complex and volatile, with the Federal Reserve maintaining a high-interest-rate stance that suppressed the release of global demand. Geopolitical conflicts persisted, and anti-globalization forces continued to rise, posing significant challenges to global free trade. Domestically, proactive fiscal and monetary policies continued to inject vitality into economic growth. However, amidst efforts to optimize balance sheets across governments, enterprises, and individuals, the issue of insufficient domestic demand became prominent. Coupled with a significant decline in real estate investment, crude steel production and steel demand declined significantly. At the same time, structural adjustments in steel demand continued, with the proportion of construction steel demand declining and that of manufacturing steel demand increasing.

Since the beginning of the year, the price of welded pipes has generally declined further, with the average price in the first half of the year shifting significantly lower. Spot profits remained low, and most welded pipe production enterprises faced losses. Small and medium-sized steel pipe production enterprises struggled, and the output and inventory of welded pipes showed a significant downward trend. In terms of capacity changes this year, China’s capacity expansion slowed down, with a noticeable increase in the elimination of capacity by small and medium-sized enterprises. Leading pipe factories, however, continued to actively expand nationwide. The significant decline in prices accelerated industry consolidation, and welded pipe production enterprises adopted a business strategy focused on controlling production, maintaining low inventory, and accelerating turnover. Meanwhile, the survival space for trading enterprises was further compressed. With the “pie” getting smaller, the vicious competition of “trading volume at the expense of price” intensified, further deteriorating the operating performance of the industry.

Looking ahead to the second half of 2024, after sufficient adjustments in the first half, the downside potential for prices is limited. In terms of demand in the second half of 2024, as newly issued special bonds gradually translate into physical work, infrastructure construction for livelihoods such as water conservancy, power, and urban pipeline renovation will become new growth drivers for steel pipe demand. Additionally, the rapid growth of steel structure output may bring sustained increases to steel pipe demand. Although real estate investment has slowed, with the progress of the “guarantee delivery” policy and the three major projects, the demand for welded pipes may still be promising.

1. Prices and Profits

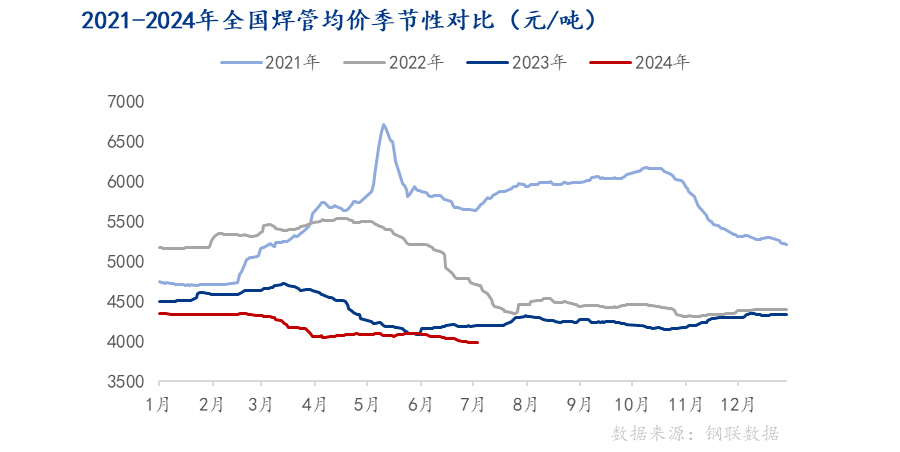

(1)Welded pipe prices declined in a step-down pattern, with average prices in the first half of the year significantly lower year-on-year

In the first half of 2024, welded pipe prices generally showed a weak trend, with an average price of 4,173 yuan/ton, a year-on-year decrease of 307 yuan/ton. After a sharp decline in March, prices remained in a narrow range of volatility, and the average price of welded pipes fluctuated between 3,950-4,100 yuan/ton in April-June.

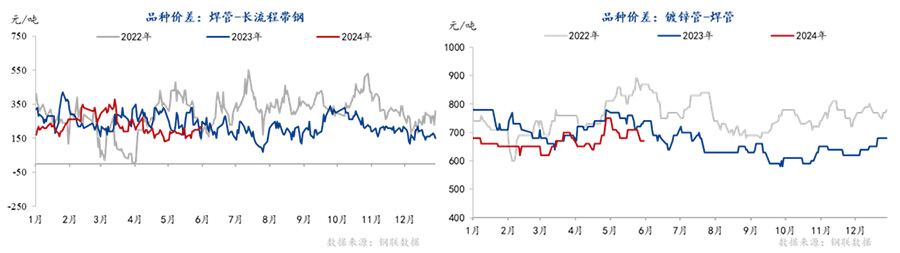

(2)The price difference between welding and galvanizing has decreased year-on-year, and there is rarely an inverted phenomenon in the coil-strip difference. The price difference between welding and galvanizing continues to narrow. In the first half of 2024, the price difference between welded pipes and galvanized pipes continued to decline year-on-year, basically stabilizing at around 660 yuan/ton, with a year-on-year contraction of about 50 yuan/ton compared to last year. The pipe-strip price difference decreased slightly year-on-year. The price difference between welded pipes and strip steel showed a trend of high in the front and low in the back, with an average price difference of 200 yuan/ton, showing a slight decrease year-on-year compared to last year. The coil-strip price difference gradually widened. Throughout 2024, the coil-strip price difference was high in the front and low in the back, with an average price difference fluctuating between 50-150 yuan/ton. In the context of relatively loose strip steel supply, the coil-strip price difference gradually widened, and the substitution benefit of hot-rolled coils was poor.

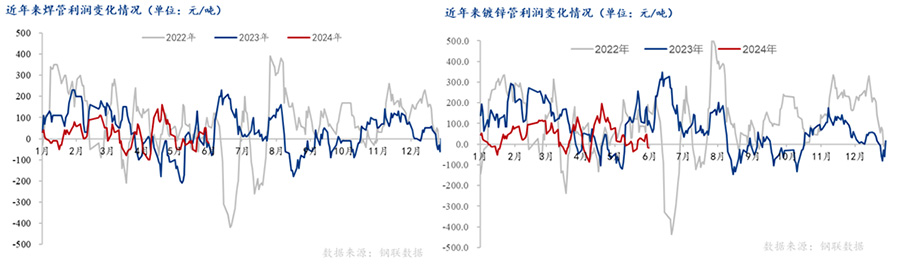

(3)The welding and galvanizing profits continue to shrink, hovering on the verge of profit and loss in the first half of the year

The profits of welded pipes and galvanized pipes continue to decline. In 2023, the average annual profit of welded pipes was 38 yuan/ton, a year-on-year decrease of 40 yuan/ton; the profit of galvanized pipes was 82.4 yuan/ton, a year-on-year decrease of 24 yuan/ton; from January to May 2024, the average profit of welded pipes was 17.4 yuan/ton, a decrease of 20.6 yuan/ton compared with 2023, and the average profit of galvanized pipes was 42.3 yuan/ton, a decrease of 40 yuan/ton compared with 2023; the number of days with immediate profit losses for welded pipes and galvanized pipes throughout the year increased significantly, and the overall operating efficiency of enterprises was poor.

2. Production and Inventory

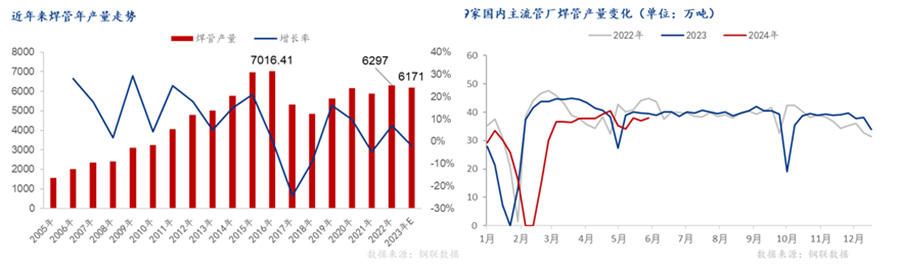

(1)Significant Year-on-Year Decline in Production in the First Half of the Year, with Notable Structural Changes in the Output of Different Product Categories

From January to June 2024, the domestic production of straight-seam welded round pipes from 29 sampled pipe factories amounted to 8.075 million tons, a decrease of 1.141 million tons or 12.4% year-on-year. Meanwhile, the production of galvanized pipes fell by 1.035 million tons, or 14.4%, to 6.152 million tons, marking a significant decline. Since 2023, there have been notable structural changes in the production of various product categories. Among the basic pipe production, while the output of rectangular pipes increased, the production of straight-seam welded pipes, spiral pipes, and scaffolding pipes declined, with the decline in straight-seam welded pipes being particularly pronounced. The proportion of high value-added products in the total output has increased significantly. For example, the share of galvanized round pipes in the total welded pipe production increased from 44.5% in 2022 to 51.7%, while the proportion of welded pipes sold outside the factories decreased significantly. Additionally, the production of galvanized rectangular pipes also increased notably. The production of traditional scaffolding pipes and disk-buckle scaffolding pipes decreased significantly due to the downturn in the real estate market.

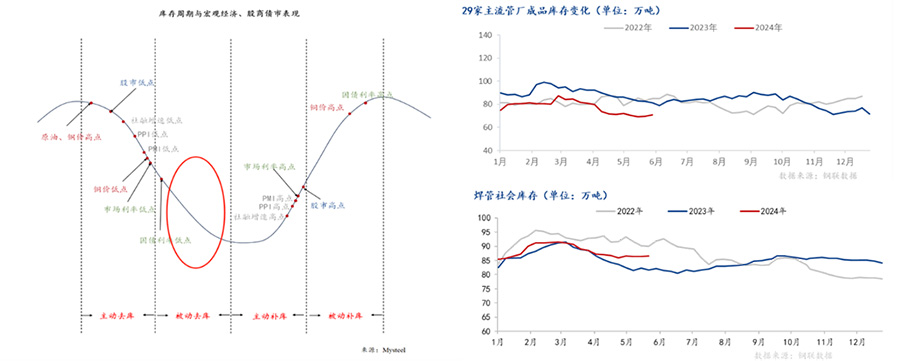

(2)Both plant and social inventories remained low during the destocking period

Pipe manufacturers produced according to sales, and inventories remained low. In the first half of the year, pipe manufacturers’ inventories decreased by about 15% year-on-year compared with 2023, basically hovering around the inventory warning line. Pipe manufacturers proactively controlled inventories to address downside price risks, and production was flexibly scheduled based on inventory levels. Trader inventories remained relatively stable. In the first half of 2024, welded pipe social inventories increased first and then decreased. Facing significant price declines, traders mostly reduced their inventories to low levels. However, due to weak demand, it was difficult to complete contractual volumes, and overall inventory declines were limited after April.

3. Demand, Imports, and Exports

(1)The pattern of low demand before and high demand after transactions weakens the transition between slack and peak seasons

Due to the significant decline in prices in the first half of 2024, the traditional “golden March and silver April” peak season failed to materialize, and overall demand was weaker than the same period last year. According to Mysteel’s statistics, the total transaction volume of welded pipes and galvanized pipes among 178 nationwide trading enterprises decreased by 21.3% year-on-year, with significant declines in the northwest and southwest regions. The decline in real estate investment has severely impacted the demand for galvanized pipes, while structural changes in demand for welded pipes remain evident. Infrastructure construction such as pipeline network renovation, power, water conservancy, and municipal guardrails has offset some of the impact of declining real estate investment. However, due to the slow pace of issuing new special bonds in the first half of the year, the overall demand for pipes has decreased significantly.

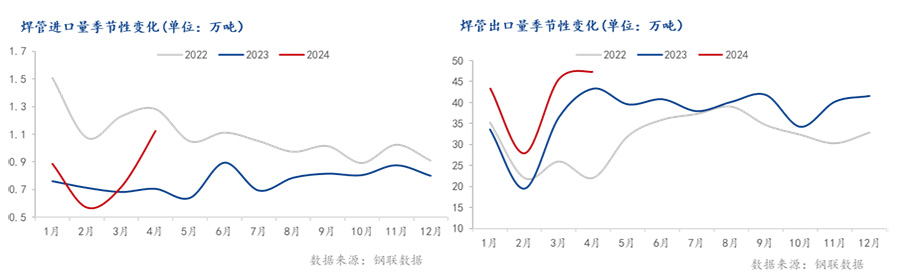

(2)Both imports and exports of welded pipes have maintained growth, and the export volume of welded pipes has reached a new high in the same period of history

China’s welded pipe exports have a strong price competitive advantage, with a significant increase in welded pipe exports. Domestic welded pipes have replaced imports, and welded pipe imports have fallen sharply. According to customs data: In May 2024, China exported 509,600 tons of welded pipes, a year-on-year increase of 28.92%; in May, China imported 11,110 tons of welded pipes, a year-on-year increase of 73.10%; from January to May 2024, China exported a total of 2,151,900 tons of welded pipes, a year-on-year increase of 24.83%; from January to May 2024, China imported a total of 44,150 tons of welded pipes, a year-on-year increase of 25.81%; from January to May 2024, China’s cumulative net exports of welded pipes were 2,107,800 tons, a year-on-year increase of 24.81.

The main export countries of welded pipes in China are the Philippines, Australia, Thailand, and Singapore, mainly developing countries in Southeast Asia and South America; The main import sources are Japan, Germany, China, and Switzerland, mainly developed countries and regions.

4. Outlook for the Welded Steel Pipe Market in 2024

(1)Macro Policy Outlook: Positive Expectations at Home and Abroad, Industrial Policies May Help the Market Rebound

In the second half of the year, industrial policies will continue to be guided by energy-saving and carbon-reduction policies. With the goals of reducing energy consumption per unit of GDP by around 2.5% and carbon dioxide emissions by around 3.9% in 2024, regulation policies on crude steel production will continue to be introduced. On the macro level, against the backdrop of China’s proactive fiscal policy and loose monetary policy, as the issuance of local government bonds accelerates and project funds are put into practice, there will be a significant boost to demand for pipes. Overseas, with the European Central Bank and the Bank of Canada leading the way in interest rate cuts, the Federal Reserve’s expected interest rate cuts in the second half of the year will further boost market confidence and have a positive impact on the market.

(2)Raw Material Market Outlook: Coal, Coke, and Iron Ore Still Face Some Risks of Decline, Prices of Coils and Strips May Follow Iron Ore Costs Closely Due to Overcapacity

Prices of coal, coke, and iron ore are still at relatively high levels historically. Under the general trend of reducing fossil fuel use, coal and coke prices may decline. The growth rate of iron water production is slow, and iron ore supply is excessive, facing certain downside risks in the long term. Coil and strip prices may be constrained by overcapacity for a long time, with weak price elasticity.

(3)Supply Outlook: Overcapacity, Increased Competitive Pressure in the Industry, Continued Compression of Small Pipe Mills’ Survival Space

The welded pipe industry will continue to undergo a reshuffle in the second half of 2024, with production declines expected to narrow slightly. Affected by the continued decline in real estate investment, the capacity utilization rate of straight seam welded pipes may continue to decline, while production of gas pipes, square and rectangular pipes, and spiral pipes may rebound. With pipe mills producing on demand and operating with low inventories, supply pressure is not significant.

(4)Demand Outlook: Demand Structure Continues to Adjust, Likely to Show Marginal Improvement in the Second Half of the Year

Currently, the number of ongoing construction sites remains high, coupled with numerous livelihood infrastructure projects such as pipeline renovations. Therefore, the availability of funds will significantly impact demand for pipes in the second half of the year. In the first four months of this year, cumulative local government bond issuance reached 2.82 trillion yuan, still lower than the 3.53 trillion yuan in the same period last year. Among them, new special bonds issued amounted to 1.07 trillion yuan (with an annual quota of 3.9 trillion yuan), accounting for 27.43% of the special bond limit. Therefore, the issuance of special bonds will further accelerate in the second half of the year. There will still be considerable demand growth in areas such as steel structures, infrastructure pipeline renovations, guardrails, water conservancy, electricity, oil and gas pipelines, and heating. The decline in real estate investment is expected to narrow further, and the decline in steel demand in the housing construction sector will have a limited impact on overall demand for pipes. Overall, demand in the second half of 2024 remains resilient, but structural changes will occur among different types of steel pipes, with square and rectangular pipes likely outperforming straight seam welded round pipes, and pipes for infrastructure projects outperforming those for real estate projects.

(5)Market Outlook: Welded Steel Pipe Prices in 2024 May Overall Show a “High at Both Ends, Low in the Middle” Trend

The annual average price of welded steel pipes is expected to decline by 150 yuan/ton. The peak price may appear in October-November, while July-August may show a bottoming-out trend with volatility. In the short term, the market is in a vacuum of demand and macro news. Amid declining demand year-on-year and seasonal weakness, pessimistic sentiment is still restraining spot price rebounds in the short term. In July, the market may maintain a bottoming-out trend with fluctuations of around 100-150 yuan/ton. In August and September, as demand improves marginally and confidence rebuilds, the market may see a rebound.